A familiar scene plays out in specialty practices every day. Your team submits a clean claim for a service you perform constantly, the EOB comes back, and the payment is nowhere near the charge or what your staff expected. The denial code may be absent. The claim may even show as “processed correctly.” But the reimbursement still feels wrong.

That gap is where a lot of revenue leakage hides.

Most providers hear insurance allowed amount and think “contracted rate.” That's only the surface. In practice, the allowed amount is the number that determines whether your claim turns into collectible revenue, contractual write-off, patient balance, appeal opportunity, or preventable loss. If your team treats it like a passive payer number instead of a controllable reimbursement lever, payers will use that passivity against you.

The problem isn't just misunderstanding the term. It's failing to police how payers apply it, change it, reinterpret it, or bury it inside payment logic that looks routine on paper. For specialty groups with high-acuity cases, multi-payer exposure, and tight margins, that mistake compounds fast.

The Hidden Meaning Behind Every EOB

A surgeon, anesthesiologist, imaging center, or ASC administrator usually doesn't start by asking, “What is the allowed amount?” They start by asking why a paid claim still looks underpaid.

That question usually begins with the EOB. The billed charge is there. The payer payment is there. Patient responsibility is there. Somewhere in that math sits the number that determined the outcome. That number is the allowed amount, whether the plan labels it that way or calls it something else.

Why this number decides profitability

The allowed amount isn't just a reimbursement detail for the billing office. It sits at the center of contract performance, coding accuracy, patient collections, and appeal strategy.

If the allowed amount is lower than it should be, your practice can lose revenue even when the claim was submitted on time and adjudicated without a formal denial. That is why payment variance review matters just as much as denial review.

A paid claim can still be a bad claim outcome.

In specialty RCM, the EOB is often the first place you see reimbursement drift. A payer starts applying a different fee schedule reference. A modifier gets ignored. A code pair gets bundled inconsistently. A claim line that should have been paid under one methodology gets processed under another. The payment posts. The underpayment hides in plain sight.

What smart teams do differently

The strongest revenue teams don't just post payments and move on. They treat every EOB as evidence.

That means they compare adjudication against contract terms, historical payment patterns, and known payer behavior. It also means the compliance side of billing can't be separated from reimbursement defense. Practices that want to tighten this process need a disciplined approach to medical billing compliance controls, because weak intake, coding, or documentation standards give payers room to push the allowed amount down.

When a practice says, “We're getting paid, but cash still feels light,” the allowed amount is usually part of the answer.

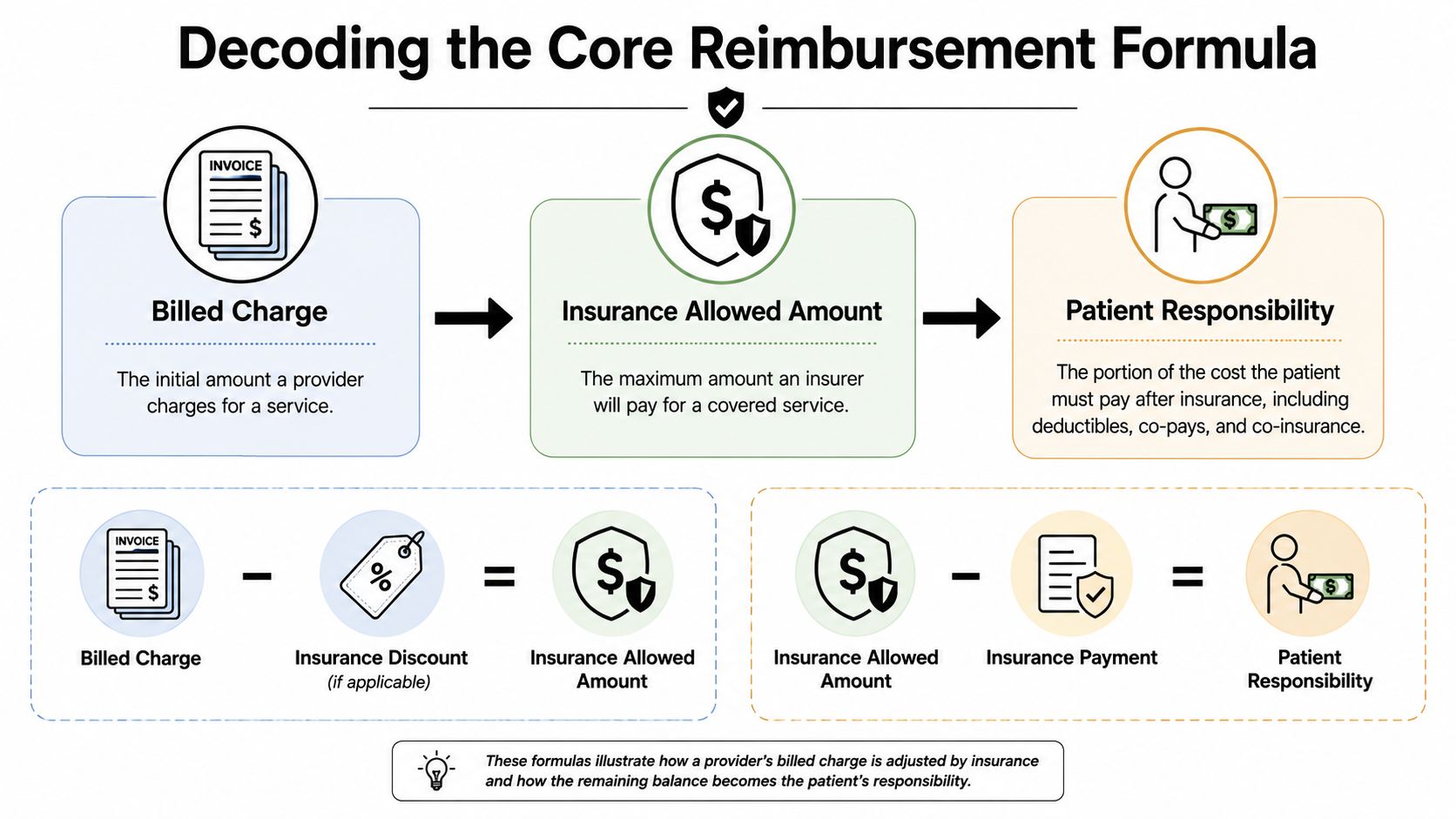

Decoding the Core Reimbursement Formula

The cleanest way to understand an insurance allowed amount is to separate it from the numbers around it.

Your billed charge is the amount your practice submits on the claim, much like the sticker price on a car. It reflects your pricing, but it doesn't automatically determine what the payer will reimburse.

The allowed amount is the maximum the plan will pay for a covered service. Federal guidance also refers to it as an eligible expense, payment allowance, or negotiated rate, as explained by HealthCare.gov's allowed amount glossary.

The simplest way to picture it

A large fleet buyer doesn't pay the same price for a vehicle that an individual consumer sees on the lot. The buyer has pre-negotiated pricing. In health care, the payer acts like that fleet buyer.

Your charge is the sticker price. The allowed amount is the pre-set price the payer recognizes for that service under the plan.

That distinction matters because reimbursement doesn't start from your charge. It starts from the allowed amount. After that, the plan applies deductible, copay, or coinsurance rules to decide who pays what.

The reimbursement math that actually matters

Here is the practical flow:

- Billed charge: What your practice submits.

- Allowed amount: The payer-recognized maximum for the covered service.

- Payer payment: The portion the insurer pays.

- Patient responsibility: The portion assigned to deductible, copay, or coinsurance.

- Write-off or balance exposure: The difference between billed charge and allowed amount, depending on network status and legal protections.

CMS explains that member cost-sharing is tied to the allowed amount, not the billed charge. In its office visit example, if the allowed amount is $100 and the member hasn't met the deductible, the member pays $100. Once the deductible is met, the member pays only the copay or coinsurance tied to that allowed amount, as outlined in CMS guidance on health insurance terms.

Why practices get tripped up

Many teams still look at paid claims through the wrong lens. They compare payment to the billed charge and assume the delta is normal because “that's just the contractual adjustment.” Sometimes it is. Sometimes it isn't.

Use this quick check:

- If the allowed amount matches the contract: the write-off may be legitimate.

- If the allowed amount is lower than contract logic supports: you likely have an underpayment issue, even if the claim shows as paid.

- If the billed charge is below the contracted allowance: your practice may have underbilled and capped its own recovery.

Practical rule: Stop asking only whether the claim paid. Ask whether it paid off the correct allowed amount.

That shift is where serious reimbursement protection starts.

How Payers Calculate Allowed Amounts

The biggest mistake providers make is assuming there's a universal allowed amount for a CPT code. There isn't.

Allowed amounts are usually shaped by payer contract terms, service type, provider credentials, and geography. The same service can pay very differently depending on which plan processed it and how that payer built its fee schedule.

The Medicare anchor and its limits

Many payers use Medicare logic as a reference point, even when they don't say so plainly. That doesn't mean they mirror Medicare. It means Medicare often acts as a baseline or negotiating anchor inside commercial reimbursement design.

One industry analysis projected that in 2026, commercial insurers will reimburse providers at an average of 196% of Medicare fee-for-service authorized amounts for overall care, while professional services will be paid at 148% of Medicare levels. The same analysis states that the Medicare physician fee schedule conversion factor was reduced by 2.83% to $32.3465, according to RCM Experts' discussion of allowed amounts in medical billing.

For providers, that matters because a payer doesn't need to rewrite your whole contract to affect reimbursement. It can shift the reference points, fee schedule logic, edit application, or interpretation around them.

What actually drives variation

A payer's allowed amount usually reflects some mix of the following:

- Contract language: The core reimbursement methodology, carve-outs, and modifier rules.

- Code-specific logic: Different handling for surgery, imaging, E/M, supplies, or ancillary services.

- Geographic adjustments: Local market conditions and payer strategy.

- Provider classification: Specialty, credentials, facility type, and network tier.

- Policy overlays: Internal edits, bundling rules, and medical necessity determinations.

This is why national averages don't help much when you're trying to validate a specific underpayment. Your practice lives inside payer-specific math, not market commentary.

Why the contract still wins

The contract is the most important reimbursement document in your revenue cycle, even when the payer tries to make payment look operational rather than contractual.

A weak contract creates downstream ambiguity. Ambiguity creates inconsistent adjudication. Inconsistent adjudication creates underpayment noise that your team may write off as routine variance.

If you run a specialty practice, don't let your team rely on broad assumptions like “this payer usually pays around Medicare plus something.” That's not enough. You need service-line-level reimbursement modeling tied to actual contract terms and actual posted payments.

The allowed amount isn't a static market fact. It's a moving payer decision with a contract wrapped around it.

In-Network vs Out-of-Network Reimbursement Impact

Network status changes the entire financial outcome of a claim, even when the underlying service is identical.

For in-network claims, the provider usually accepts the allowed amount as full contractual payment and writes off the difference between the billed charge and the allowed amount. For out-of-network claims, that difference can become a patient balance if balance billing is permitted. CMS notes an example where a $100 billed charge with a $70 allowed amount can leave the patient responsible for the remaining $30 if balance billing is allowed, as summarized in this overview of allowed amounts and network status.

What changes when you're in network

In network, your main risk isn't usually balance billing. It's accepting a payer's adjudication without validating whether the allowed amount was calculated correctly under the contract.

Your contract controls the write-off. If the payer applies the wrong fee schedule, ignores a carve-out, or misclassifies the service, the underpayment gets buried inside what staff may post as a normal contractual adjustment.

What changes when you're out of network

Out of network, the allowed amount still matters, but the dispute profile changes.

Now the practice has to think about plan payment, patient exposure, state and federal protections, and whether the claim falls into a lane where further enforcement is available. Teams that handle these claims well usually build distinct workflows for out-of-network reimbursement and benefits recovery, because the playbook isn't the same as ordinary in-network follow-up.

Side-by-side comparison

| Metric | In-Network Scenario | Out-of-Network Scenario (No NSA Protections) |

|---|---|---|

| Contract relationship | Direct payer-provider agreement controls reimbursement | No direct in-network contract controls reimbursement |

| Allowed amount role | Sets the maximum payable amount under the contract | Sets plan payment logic but may not limit total provider charge |

| Difference between billed charge and allowed amount | Usually written off by provider as contractual adjustment | May become balance-bill exposure if permitted |

| Main provider risk | Underpayment hidden inside “contractual” posting | Low plan payment plus collection friction and patient dissatisfaction |

| Main patient risk | Deductible, copay, or coinsurance based on plan rules | Potential cost-sharing plus billed balance if protections don't apply |

| Best operational defense | Contract modeling and underpayment audits | Eligibility review, legal pathway analysis, and escalation readiness |

Out-of-network claims can produce higher gross charges on paper and worse cash outcomes in reality.

The operational takeaway

Practices often focus on whether joining a network increases volume or depresses rates. That's only part of the decision. The more useful question is this: where does your team have the best ability to validate, enforce, and recover the correct payment?

In network gives you contractual predictability, but only if you audit it. Out of network may preserve an advantage in some circumstances, but only if your intake, documentation, and dispute escalation process are strong enough to support it.

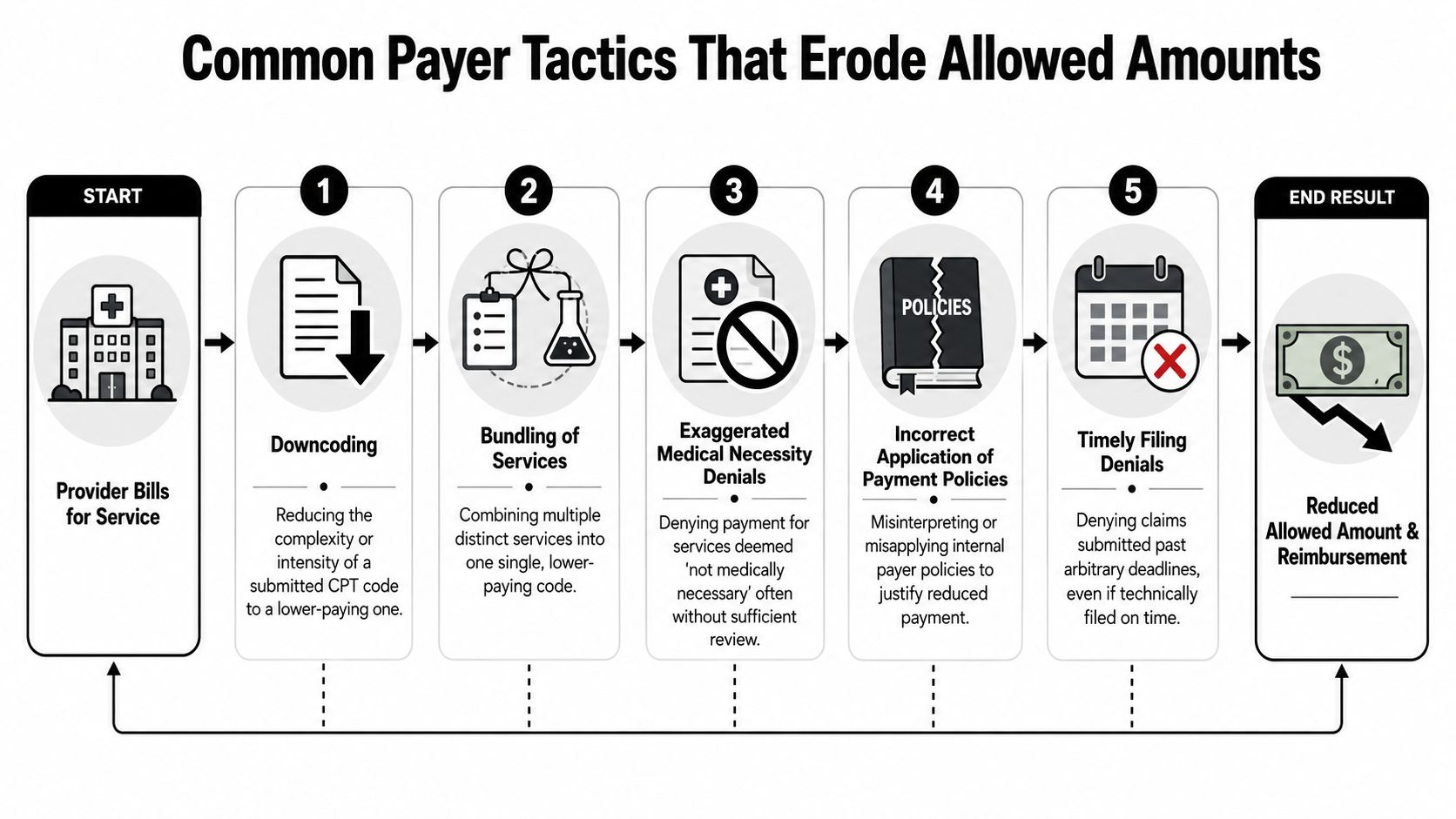

Common Payer Tactics That Erode Allowed Amounts

Most underpayments don't arrive with a note that says, “We chose to reimburse you less.” They show up as ordinary claims activity.

That is why providers miss them. The tactic isn't always a blunt fee cut. It's usually a quieter move that lowers the effective allowed amount, narrows the payable service mix, or shifts dollars out of insurer liability and into write-offs or bad debt.

The tactics that hit specialty practices hardest

A recent industry-specific example notes that the 2026 physician fee conversion factor is $32.35, a 2.83% decrease from the prior year, which shows how even small payment-policy changes can alter allowed amounts and downstream revenue, as discussed by Avenue Billing Services in its allowed amount analysis. That same dynamic plays out inside commercial adjudication. Small policy shifts create real payment drift.

Here are the payer moves revenue teams need to watch:

- Downcoding: The payer changes the submitted code to one that pays less. The claim may still be marked paid, but the allowed amount now attaches to a lower-valued service.

- Bundling: Separate services that should reimburse independently get collapsed into one lower-paying line item.

- Medical necessity pressure: The payer uses internal criteria to narrow payable coverage after the service is already performed.

- Policy misapplication: A valid modifier, place-of-service rule, or specialty carve-out gets ignored.

- Timely filing technicalities: The payer uses submission timing or documentation defects to avoid full adjudication.

Why these tactics are so effective

They work because they look administrative.

A practice may train staff to chase denials but not to analyze paid claims. That leaves a blind spot. The payer doesn't need to deny the entire claim if it can alter one code, recategorize one line, or apply one edit that brings reimbursement down while preserving the appearance of normal processing.

If your team reviews denials but not paid-claim variance, you're only seeing part of the leakage.

Silent discounting and reimbursement drift

Another issue providers underestimate is discount creep. Sometimes the allowed amount starts diverging from contract intent gradually, not suddenly. A payer changes edit behavior on one service family. Then another. Then a modifier pattern starts paying differently than it did in prior months.

Specialties with repeatable service mixes feel this first. Anesthesia groups, imaging centers, emergency providers, orthopedics, and procedure-heavy practices usually have enough volume for drift to become visible. But visibility only matters if someone is measuring.

What doesn't work is anecdotal monitoring. “This payer feels lighter lately” isn't an audit method.

What works is line-level comparison against contract logic, historical payment behavior, and known reimbursement rules. Once a payer knows a practice can't or won't challenge low allowed amounts consistently, the underpayment pattern usually spreads.

A Proactive Playbook to Protect Reimbursement

Revenue protection starts long before the appeal letter.

If your practice waits until underpayments show up in aging reports, you've already lost time, cash, and advantage. The stronger approach is to build controls upstream so the claim leaves the practice with the best possible reimbursement posture and comes back easy to validate.

Tighten contract modeling before claims hit the payer

Payer-by-payer variation creates a hard ceiling on reimbursement. If your charge master sits below the highest contracted allowed amount, the payer will usually pay only up to the submitted billed charge, not above it. That means a practice can negotiate a stronger rate and still fail to collect it if charges are set too low, as explained in this discussion of billed amounts versus allowed amounts.

Many specialty groups lose money. They focus on fee schedule language but don't reconcile that language to actual billed charge floors.

Use this checklist:

- Model each payer separately: Don't average contracts together. The reimbursement logic is too different.

- Compare billed charges to top allowed amounts: Make sure you aren't capping your own collection.

- Flag vague contract language: “Usual policy,” “payer discretion,” and undefined edit references create downstream ambiguity.

- Track carve-outs carefully: High-cost or specialty-heavy code families often live in exceptions, not main fee schedules.

Clean up coding and charge capture discipline

Payers exploit inconsistency. If the same service is coded differently across locations, providers, or billers, the payer gets room to apply edits unevenly.

Coding hygiene isn't just a compliance issue. It's reimbursement defense. Specialty practices need code selection consistency, modifier discipline, documentation that supports intensity, and fast feedback loops between coders and payment posters.

A few practical habits help:

- Review top revenue codes monthly. Not every code. The codes that move cash.

- Separate denied claims from underpaid claims. They need different owners and different workflows.

- Audit modifier-sensitive services. That's where many payment reductions hide.

- Map payer edits by specialty. A generic denial matrix won't catch specialty-specific erosion.

Build an underpayment process, not a reactive appeal pile

Most practices have an appeals process. Fewer have a real underpayment enforcement process.

Those are not the same thing.

An effective underpayment workflow includes:

- Expected payment logic: What should this claim have paid under contract or known reimbursement rules?

- Variance triggers: Which dollar gaps, service lines, or payer patterns require review?

- Evidence capture: EOB, contract language, coding support, medical record support, and historical comparison.

- Escalation rules: Front-end correction, reconsideration, formal appeal, legal review, or dispute action.

Operational rule: Don't let staff post a “contractual adjustment” unless someone has validated the contract math.

What works and what doesn't

What works

- Service-line benchmarking by payer

- Charge floor reviews tied to real contracted allowances

- Payment posting teams trained to spot variance, not just close encounters

- Appeals grounded in contract language and claim-specific evidence

- Cross-functional reviews between coding, contracting, and AR follow-up

What doesn't

- Looking only at denial rates

- Assuming paid claims are correct

- Treating all payer issues as “billing problems”

- Leaving contract interpretation to the payer's EOB language

- Waiting until annual contract renewal to investigate reimbursement drift

The allowed amount is where payer strategy meets your operational discipline. If your systems don't catch variance early, the payer's version of the contract becomes the one that gets enforced.

Advanced Defense IDR and Monitoring Key KPIs

Some claims won't resolve through ordinary appeals. That's where enforcement has to become part of the revenue cycle.

For eligible out-of-network claims and certain No Surprises Act scenarios, the Independent Dispute Resolution process can become a serious recovery tool when the payer refuses to move. The key is that IDR works best when the claim enters that stage already built for dispute. Weak intake, weak coding, and weak payment analysis usually produce weak escalation.

Practices that want to connect daily RCM controls with formal dispute advantage need a process similar to the one outlined in this breakdown of how RCM and IDR work together.

The KPIs that actually expose allowed amount problems

Don't drown your team in dashboards. Watch the metrics that reveal reimbursement erosion fastest:

- Allowed amount by payer and code family: Spot drift before cash drops materially.

- Payment per unit of service: Useful for repeatable specialty procedures.

- Underpayment rate by payer: Separate from denial rate.

- Appeal overturn patterns: Shows where payer behavior is systemic.

- Days in A/R by payer segment: Delays often accompany contested reimbursement.

- Write-off patterns: Contractual write-offs should be predictable. If they aren't, investigate.

When to escalate

Escalation makes sense when a payer's behavior is repeatable, materially harmful, and resistant to ordinary correction. That may mean repeated low allowed amounts, misapplied payment logic, or out-of-network payments that require formal challenge.

The broader point is simple. A practice protects reimbursement when it treats the allowed amount as something to verify, monitor, and enforce, not just post.

RevGuard helps provider groups, ASCs, hospitals, and multi-state specialty platforms protect reimbursement by combining specialty-focused RCM with enforcement-driven IDR under the No Surprises Act. If your team is dealing with chronic underpayments, reimbursement drift, or payer behavior that keeps slipping past ordinary billing workflows, RevGuard can help turn those claims into a disciplined revenue protection process.