An out of network claim lands in your work queue. The case was legitimate, the documentation is solid, the coding is supportable, and the payer still sends a payment that bears little resemblance to the value of the service. The old playbook would have pushed the gap toward the patient. In many specialties, that playbook is gone or sharply limited.

That's the operating reality now for anesthesia groups, surgical specialists, air ambulance providers, hospital-based physicians, and other practices that still depend on out of network reimbursement. The issue isn't whether out of network benefits exist on paper. The issue is whether those benefits translate into collectible revenue after plan design, payer edits, statutory protections, and payment disputes all take their turn.

For specialty practices, the work has shifted. Protecting revenue now depends less on balance billing and more on building claims that can survive scrutiny, appeals, negotiation, and, when necessary, formal dispute resolution.

The Reality of Out of Network Reimbursement

A common specialty-practice scenario looks like this. You treat the patient, bill the claim correctly, and receive an out of network payment based on an internal payer methodology you never agreed to. The remittance offers little transparency. The patient can't absorb the difference, or federal rules bar balance billing altogether. Your revenue team is left deciding whether to write it off, appeal it, or escalate it.

That scenario matters because out of network reimbursement hasn't gone away. It has become narrower, more contested, and more operationally demanding. In a large commercial claims study, the share of total healthcare spending that occurred out of network fell from 7.0% in 2008–10 to 6.1% in 2014–16, yet 10.6% of cost-sharing was still attributable to out of network care, according to a commercial claims analysis published in Health Affairs Scholar via PMC.

Why the pressure feels worse now

Many practices see the same pattern repeatedly:

- Payment arrives low: The initial allowed amount reflects the payer's view of the service, not the provider's billed charge.

- Patient collection is limited: In protected scenarios, the patient's responsibility is restricted.

- Appeals consume staff time: Teams spend hours assembling records, correspondence, and payment comparisons.

- Cash flow slows down: The longer the dispute sits unresolved, the harder monthly performance becomes to manage.

Practical rule: If your out of network strategy still depends mainly on collecting the gap from patients, your process is out of date.

The core problem isn't just that payers underpay. It's that many specialty groups still treat out of network claims as exceptions when they should be treated as a distinct reimbursement channel with its own workflow, evidence standards, and escalation path.

What actually works

Practices do better when they stop treating out of network claims like ordinary fee-for-service submissions. These claims need front-end verification, clean documentation, strong coding discipline, payer-specific follow-up, and a clear threshold for when an underpayment becomes a formal dispute.

That change in mindset is the difference between reacting to isolated shortfalls and managing out of network benefits as a revenue system.

Defining In Network vs Out of Network Benefits

The simplest way to explain the difference is to think about a preferred auto repair shop versus one your insurer doesn't recognize. At the preferred shop, the pricing framework is already set. At the non-preferred shop, you may still have coverage, but the rules are looser, reimbursement is less predictable, and your share of the bill can rise fast.

Healthcare works the same way. In-network means the provider has a contract with the payer. Out-of-network means there is no contract governing reimbursement terms. That single difference affects every downstream payment question.

What changes when the provider is out of network

With in-network care, the payer and provider have already negotiated rates, billing rules, and administrative expectations. The provider knows the contract structure. The patient usually has a more predictable benefit design.

With out of network care, the plan may still offer a benefit, but the financial structure is often much harsher. A benefits guide describing common plan patterns notes that out of network coverage often involves a separate deductible, lower reimbursement after deductible, and exposure to balance billing above the insurer's allowed amount in this explanation of in-network versus out-of-network plan mechanics.

That's why the phrase out of network benefits can mislead patients. A benefit can exist while still leaving the patient with major liability.

The plan structure providers need to explain clearly

| Feature | In-Network | Out-of-Network |

|---|---|---|

| Contracted rate | Yes | No |

| Deductible structure | Usually integrated with plan design | Often separate and harder to satisfy |

| Cost sharing after deductible | Typically more favorable | Often less favorable |

| Out-of-pocket exposure | More predictable | Can be significantly higher |

| Balance billing risk | Generally limited by contract terms | May apply unless prohibited by law |

| Payment flow | Direct and more standardized | Often delayed, partial, or disputed |

A second issue is access to the benefit itself. In the individual market, the share of plans offering out of network coverage dropped from 58% in 2015 to 29% in 2018. Among plans that did offer it, the median out of network deductible was about $12,000, and about 30% had deductibles above $20,000, based on a Robert Wood Johnson Foundation analysis of out-of-network benefits in marketplace plans.

What providers should say to patients

Patients often ask one question: “Do I have out of network coverage?” That's not enough. The more useful questions are:

- Is there a separate deductible? A yes answer changes the patient estimate immediately.

- What is the reimbursement basis? Plans may pay on an internal allowed amount that differs sharply from the provider's charge.

- Does the law limit what the patient owes? That determines whether the issue is patient responsibility or payer reimbursement.

- Will the claim be assigned or patient-filed? That affects timing, follow-up, and collection risk.

Out of network isn't just a network label. It's a different reimbursement environment with different collection odds.

Practices that explain this well reduce confusion later. Practices that don't often find themselves trying to fix a financial misunderstanding after the service is complete.

How OON Status Impacts Providers and Patients

For providers, out of network status creates operational drag before it provides legal advantage. The claim is more likely to require manual benefit review, customized estimate work, additional documentation, and follow-up that can't be automated as cleanly as contracted claims. That burden doesn't show up on the EOB, but it hits staffing, aging, and write-offs.

For patients, the impact is less about abstract coverage and more about timing and uncertainty. Even when a plan technically includes out of network benefits, the patient may face a separate deductible, a lower reimbursement percentage, or a reimbursement path that requires waiting for the payer to process a claim before anyone knows what the actual out-of-pocket amount will be.

Why this keeps happening in facility-based care

Out of network exposure is common in the settings where many specialty practices work. In large employer plans, nearly 18% of inpatient admissions included at least one out of network claim, and 7.7% of outpatient service days did as well. Even when patients used an in-network facility, 15.4% of inpatient admissions still involved an out of network claim, according to a Health System Tracker analysis of out-of-network claims in large employer plans.

That pattern matters for anesthesiology, surgical assist, radiology, pathology, emergency medicine, neonatal care, and similar specialties. The facility may be in network while one of the clinicians billing separately is not. From the patient's perspective, the distinction is confusing. From the provider's perspective, it creates reimbursement friction that starts after care has already been delivered.

The operational consequences inside the revenue cycle

Revenue teams usually feel out of network pain in four places:

- Verification failures: Staff confirm eligibility but don't fully map the out of network structure, especially when the plan has separate cost-sharing rules.

- Underpayment reviews: Low allowed amounts are posted before anyone has determined whether the payment is defensible.

- Patient collections: Statements go out with balances the patient doesn't understand or shouldn't owe in the first place.

- Aging and rework: Appeals, corrected claims, and payer calls pile up around the same carriers.

A separate challenge is that out of network claims often invite more payer discretion. The plan may rely on opaque payment logic, claim edits, or internal reimbursement thresholds that the provider didn't negotiate and can't easily validate.

The real cost of out of network care is often administrative first, financial second.

When practices ignore that, they measure only the payment shortfall and miss the labor cost, delay cost, and downstream bad debt attached to the same claim.

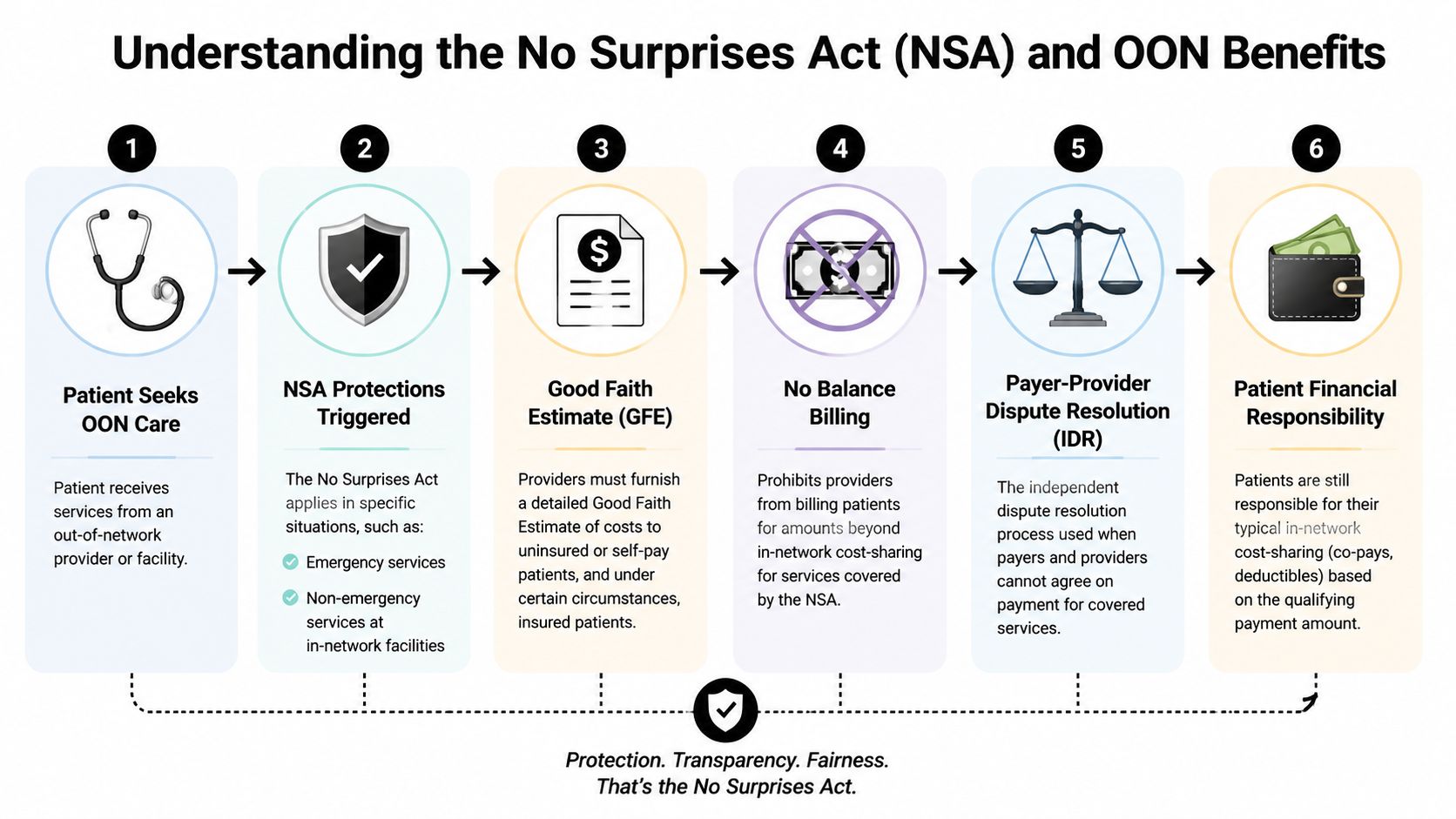

The No Surprises Act and Its Effect on OON Care

The No Surprises Act didn't make out of network status disappear. It changed who carries the dispute. In many emergency and certain non-emergency situations, the patient is no longer the pressure point. The payer is.

The practical shift is straightforward. When the law applies, providers generally can't rely on surprise balance billing to recover the gap between billed charges and the payer's initial payment. A neutral overview notes that the No Surprises Act limits patient cost-sharing and bans balance billing in many emergency and certain non-emergency cases, shifting the conflict to payer-provider resolution and making IDR the main formal path for challenging inadequate payment in this summary of No Surprises Act protections.

When the law changes the claim path

Protected claims now follow a different financial logic:

- The patient receives care in a setting covered by the statute.

- The patient's financial responsibility is limited to applicable in-network cost-sharing.

- The provider receives an initial payment or denial from the payer.

- If the amount is inadequate, the provider challenges the payment through the statutory process instead of billing the patient for the unrestricted balance.

That's a structural change, not a billing nuance.

Why IDR matters more than balance billing now

For many specialty groups, Independent Dispute Resolution is the new pressure valve. The argument is no longer “Can we bill the patient for the rest?” The argument is “Can we prove the payer's payment is not appropriate for this service, this level of complexity, and this market context?”

That's especially important in emergency-linked specialties and transport settings. Air ambulance providers, for example, operate in a part of the reimbursement environment where federal protections and dispute rules are central to revenue strategy. Teams working through those issues often need a separate workflow for protected transport claims, as outlined in this air ambulance No Surprises Act overview.

What practices should operationalize

The No Surprises Act forces a tighter link between compliance and reimbursement. To function well under the statute, practices need to operationalize:

- Accurate identification of protected claims

- Clean calculation of patient responsibility

- Consistent preservation of records that support payment disputes

- Timely escalation when an initial payment doesn't reflect the case

If your staff can identify a protected claim but can't assemble a persuasive payment challenge, you're compliant but still exposed.

The providers doing this well don't treat IDR as an occasional legal remedy. They build workflows around it from the start.

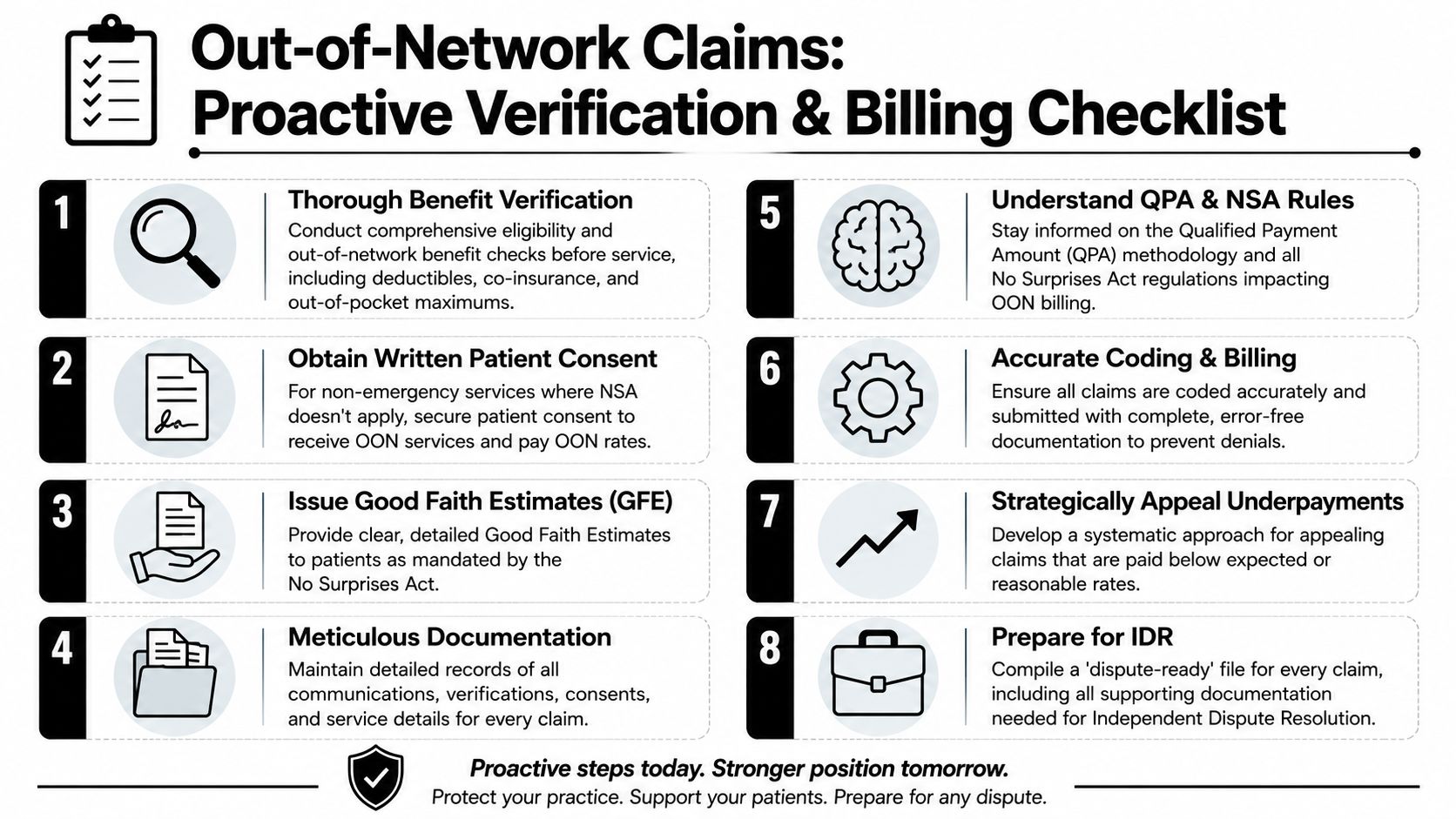

Proactive Verification and Billing Best Practices

Most out of network disputes are won or lost before the first claim is submitted. If the intake team misses the benefit structure, if the estimate is vague, or if the chart and claim don't tell a coherent story, the back end has to fight with weak evidence.

That's why the right goal isn't just a clean claim. It's a dispute-ready claim.

Front-end controls that prevent expensive mistakes

Pre-service work has to go beyond basic eligibility. A proper out of network intake process should answer not only whether coverage exists, but how the plan treats the claim financially and whether the service may fall under federal protections.

A strong workflow usually includes:

- Deep benefit verification: Confirm network status, separate out of network deductible structure, cost-sharing terms, and whether the patient's financial exposure is limited by law. Teams that need a tighter intake workflow often use a dedicated medical eligibility verification process rather than relying on generic scheduling scripts.

- Patient financial communication: Give the patient a plain-language explanation of what is known, what is uncertain, and what may depend on payer adjudication.

- Written consents and estimates: Use documents that align with the service setting and the legal rules. The form should support collections and compliance, not just paperwork completion.

Back-end habits that strengthen payer disputes

Once the service is delivered, the file needs to support the medical necessity, coding accuracy, and reimbursement argument without forcing your appeals team to rebuild the story from scratch.

The claims with the best recovery potential usually share the same features:

- Coding matches the record: Modifiers, place of service, provider identifiers, and claim form details all align with the chart.

- Documentation supports complexity: The record explains why the service required this provider, this level of skill, this setting, and this intensity.

- The billing packet is complete early: Intake notes, authorizations if applicable, consent records, operative or procedural notes, and payer communications are all easy to retrieve.

A practical checklist for specialty groups

Use this checklist to test whether your operation is ready for out of network reimbursement disputes:

- Before service: Verify the benefit structure, not just active coverage.

- At scheduling or registration: Flag whether the claim may be NSA-protected.

- Before claim submission: Audit coding and documentation for consistency.

- After payment posts: Review underpayments against expected reimbursement logic, not just against whether anything was paid.

- Before escalation: Build one file that another team member could defend without chasing missing records.

Practices that do this well reduce avoidable denials. They also move faster when a claim needs formal escalation because the support file already exists.

Payer Negotiations and IDR Strategy for Underpayments

Accepting a low initial payment because it seems faster is one of the most expensive habits in specialty revenue cycle work. Payers learn quickly which groups escalate and which groups don't. If your team rarely challenges underpayments, the carrier has little reason to improve its offers voluntarily.

The better approach is an enforcement mindset. Not a chaotic appeal culture. A disciplined one.

What a strong underpayment strategy looks like

A practice that consistently recovers more from out of network claims usually has three things in place.

First, it tracks payer behavior at the claim-family level. One low payment might be an anomaly. A repeated pattern tied to a payer, service line, or market is a strategy by the carrier and should be managed that way.

Second, it separates technical denials from payment-value disputes. A missing modifier issue and a reimbursement adequacy issue are not the same problem. They need different workflows, timelines, and staff skills.

Third, it develops evidence templates for recurring claim types. That means your team isn't reinventing the case every time an anesthesia claim, emergency consult, or transport episode is underpaid.

What makes an IDR argument persuasive

The strongest payment disputes don't just say the payer paid too little. They explain why the service justifies more.

Useful evidence often includes:

- Case-specific complexity: The record should show acuity, unusual clinical demands, or service intensity where applicable.

- Provider qualifications and role: Specialty expertise, call burden, and facility-based obligations may matter depending on the claim type.

- Clean chronology: The timeline from service to billing to payment to challenge should be easy to follow.

- Consistent internal reasoning: Your billed amount, appeal position, and supporting documents should tell the same story.

A weak dispute file contains documents. A strong dispute file makes a payment decision look unreasonable.

Build negotiation pressure before formal escalation

Not every underpayment needs to go straight into the same path. Some should be appealed conventionally first, especially when the payer's own processing appears defective. Others should move quickly into a more formal reimbursement challenge because the issue is not an error but a systematically low valuation.

That's where disciplined denial and underpayment management matters. Teams often need a structured healthcare denial management workflow that separates recoverable technical issues from broader payer reimbursement disputes. In some organizations, platforms such as RevGuard are used to connect front-end RCM work with downstream IDR preparation so the evidence assembled at intake and billing can be reused when the payer's payment is challenged.

What does not work

Several habits consistently diminish advantage:

- Posting and forgetting: If payment posts without variance review, the underpayment becomes a write-off by default.

- Generic appeal letters: Boilerplate language rarely moves a payer or supports later arbitration.

- Late evidence gathering: If records, estimates, consent documents, and communications are scattered, the dispute starts from a position of weakness.

- Treating every claim the same: A protected emergency claim, a voluntary out of network elective case, and a facility-based surprise-billing scenario should not all follow one script.

The point isn't to fight every payment. It's to contest the ones that matter using a process that can scale.

Conclusion Protecting Revenue in the New OON Landscape

Out of network benefits still matter, but the economics have changed. For many specialty providers, the old model relied on patient exposure to close the reimbursement gap. The current model relies on operational discipline, legal awareness, and the ability to challenge payer payments effectively.

That shift changes what “good revenue cycle management” means. It now includes identifying protected claims correctly, verifying the actual benefit structure before service, documenting the case in a way that supports reimbursement, and escalating underpayments with purpose instead of frustration.

The practices that protect revenue in this environment don't wait for payer behavior to improve. They build systems that assume low initial payments will happen. Then they respond with better intake, cleaner billing, stronger evidence, and a repeatable dispute process.

That's the new out of network playbook. It's less about chasing patients and more about confronting underpayment where it starts. With the right process, out of network reimbursement becomes manageable again, even in a market where payer pressure is constant and statutory rules have changed the collection path.

RevGuard helps provider groups, hospitals, ASCs, and specialty practices connect front-end revenue cycle work with post-payment enforcement under the No Surprises Act. If your team is dealing with recurring out of network underpayments, IDR volume, or weak claim documentation that hurts appeals, RevGuard is one option to evaluate for building a more dispute-ready reimbursement process.