Monday starts with a familiar escalation. A patient had emergency care, your clinicians did the work, the claim went out clean, and the payer's response still doesn't match the service you delivered. Before the law changed, that gap often landed in the patient's mailbox as a balance bill, and then in your office as a complaint, a write-off decision, or both.

Most practice administrators don't need another high-level legal explainer. They need a No Surprises Act summary that connects the statute to cash flow, payer behavior, staff workflow, and recoverability. That's where the main challenge sits now.

Since January 1, 2022, the No Surprises Act has shifted many surprise-billing disputes away from patients and into a formal payment process between providers and health plans, including open negotiation and, when needed, binding independent dispute resolution for covered claims, as outlined in CMS guidance on key NSA protections. For providers, that means reimbursement discipline matters more than ever. You can't rely on old billing habits, and you can't afford to treat underpayments as isolated exceptions.

The End of Surprise Billing as We Knew It

For years, out-of-network reimbursement followed a predictable pattern in many specialties. The patient received care in circumstances they didn't fully control, the payer issued a low payment or denial, and the provider was left deciding whether to pursue the patient, fight the insurer, or absorb the loss. Emergency medicine, anesthesiology, radiology, pathology, and air ambulance providers know that cycle well.

That model is gone for many federally protected situations. The No Surprises Act replaced the old pressure point. Patients generally aren't the collection target for covered services anymore. The dispute now sits where it should have been all along, between the provider and the payer.

What changed in practical terms

The law applies broadly, not just to a narrow insurance segment. It covers most consumers in employer plans, Marketplace plans, and individually purchased health insurance. It also bars balance billing for covered services in the settings the statute protects, while limiting patient cost-sharing to in-network levels for those claims.

That sounds like a compliance story. It's also a revenue story.

When patient billing is restricted, every weak handoff inside the revenue cycle gets exposed faster:

- Registration errors can misclassify the claim and delay payment strategy.

- Posting mistakes can hide an eligible underpayment.

- Appeal lag can cause the practice to miss its advantage during negotiation.

- Poor documentation can leave a recoverable claim unsupported when payment is challenged.

Covered claims no longer give providers much room for passive revenue recovery. If the payer underpays, the file has to be ready for dispute.

A good No Surprises Act summary for providers has to start there. This isn't just a patient-protection law. It's a reimbursement framework that rewards organized groups and punishes loose operational habits.

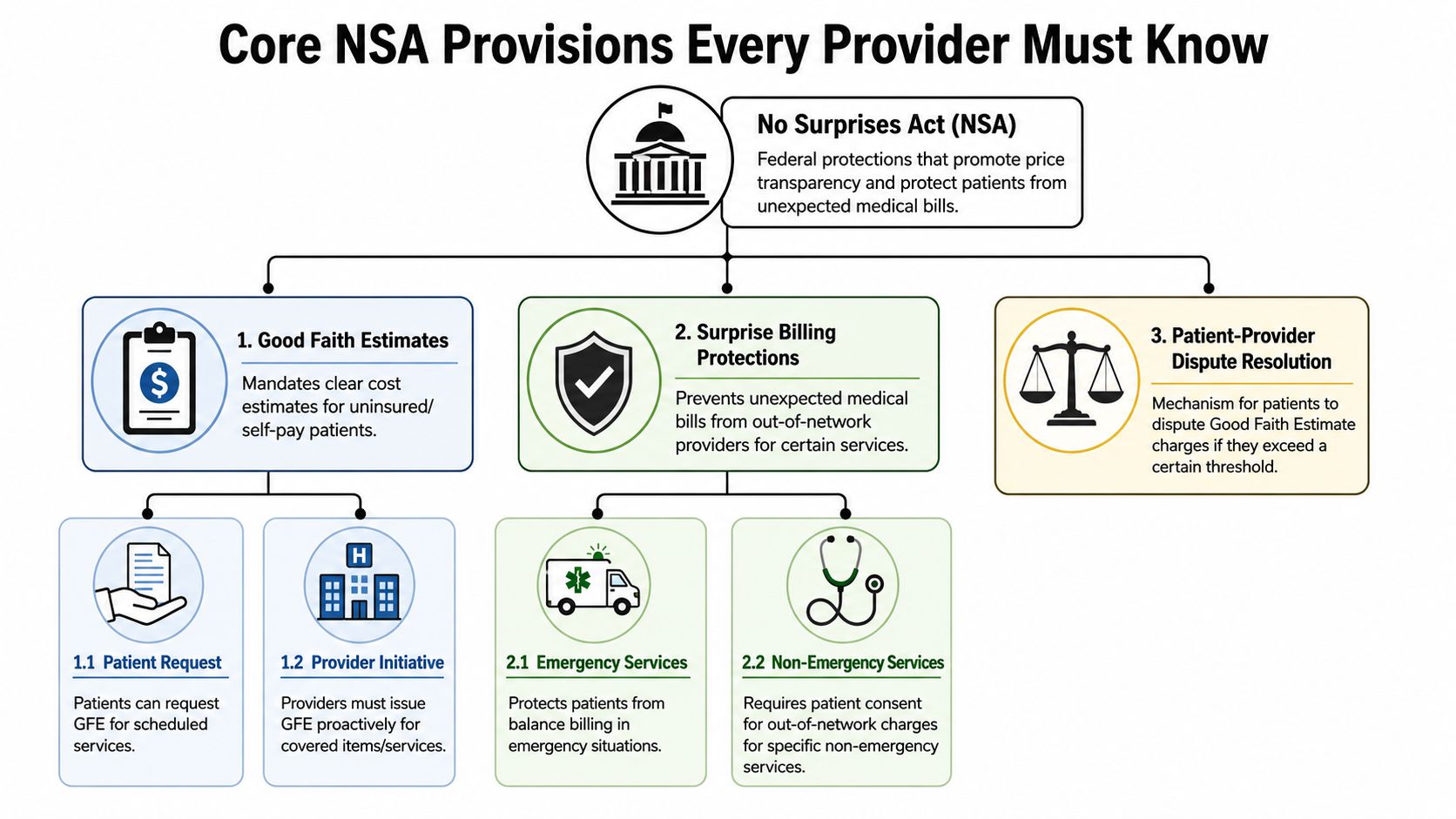

Core NSA Provisions Every Provider Must Know

The statute is easiest to manage when you reduce it to three practical rules: where it applies, what you can't bill, and how the patient's share is limited. If your staff can answer those three questions correctly at intake, claim creation, and payment review, you've already reduced avoidable risk.

The protected settings

At a high level, the NSA protects patients in three major categories of care:

- Emergency services where the patient typically can't choose the treating clinician in a meaningful way.

- Certain out-of-network services at in-network facilities where the facility may be in network but a facility-based clinician is not.

- Out-of-network air ambulance services that fall within the federal protection structure.

These protections are part of the federal framework described in the earlier-cited CMS guidance. In day-to-day operations, that means schedulers, front-desk staff, and billing teams need to identify not only network status, but also the care setting. The setting often determines whether normal out-of-network collection logic is prohibited.

The balance billing ban

For covered services, providers generally can't balance bill the patient. That's the operational line that matters most. If your team still follows old workflows that automatically route residual balances to patient statements, you create both compliance exposure and patient-relations damage.

The safer approach is to build a claim-edit or workqueue rule that flags likely NSA claims before patient billing begins. That's especially important for specialties that deliver care at hospitals, ASCs, and emergency settings where the patient may never have made an informed provider selection.

In-network cost-sharing still applies to the patient

Patients in protected scenarios generally owe only the in-network cost-sharing amount for the covered service. That means copay, coinsurance, and deductible treatment should align with in-network expectations, even when the rendering provider is out of network under a protected fact pattern.

A lot of leakage starts when teams understand this rule conceptually but don't operationalize it. They know the patient shouldn't receive the full residual balance, but they don't have a dependable workflow for stopping statements and rerouting the balance into payer follow-up.

Here's the practical distinction:

| Issue | What works | What fails |

|---|---|---|

| Claim identification | Flag protected claims early based on setting and service type | Reviewing eligibility only after patient complaints |

| Patient statements | Hold balances until NSA review is complete | Sending bills first and correcting later |

| Underpayment follow-up | Route to payer dispute workflow | Treating the payment as final because patient billing is blocked |

For groups that still struggle with out-of-network classification and reimbursement logic, a solid understanding of out-of-network benefits workflow helps connect front-end eligibility with backend payment strategy.

The Notice and Consent Exception Explained

A common misunderstanding is that the NSA erased every form of out-of-network patient liability. It didn't. What it did was make the exception narrow, technical, and risky to misuse.

Why this exception isn't a loophole

Some providers assume a signed form solves the problem. Usually, it doesn't. The notice and consent pathway is limited, and it's a bad place for casual workflow. If your team treats it like a general waiver process, you're inviting disputes over whether the patient's consent was valid, informed, and timely.

For practical purposes, administrators should think of notice and consent as an exception that requires disciplined controls, not as a fallback revenue tool.

If your staff can't explain exactly when notice and consent is allowed, they shouldn't be using it.

Where provider groups get into trouble

The biggest errors are operational, not theoretical:

- Using generic forms that don't match the service, setting, or timing requirements

- Collecting signatures too late in the scheduling or treatment process

- Applying consent logic to services that are functionally protected

- Failing to preserve documentation in a way that can support later review

Ancillary and facility-based specialties face the highest risk here because many of the services patients receive in those settings aren't realistically shoppable from the patient's perspective. That's why administrators should be skeptical whenever someone says, “We'll just have the patient sign.”

A safer administrative stance

Use notice and consent sparingly. Require legal and revenue cycle alignment on the form, workflow, storage, and audit trail. If your group can't show exactly when the notice was delivered, what the patient was told, and why the service qualifies for the exception, assume the protection applies and pursue the payer, not the patient.

That approach feels conservative. In practice, it protects revenue by preventing invalid balances that later have to be reversed.

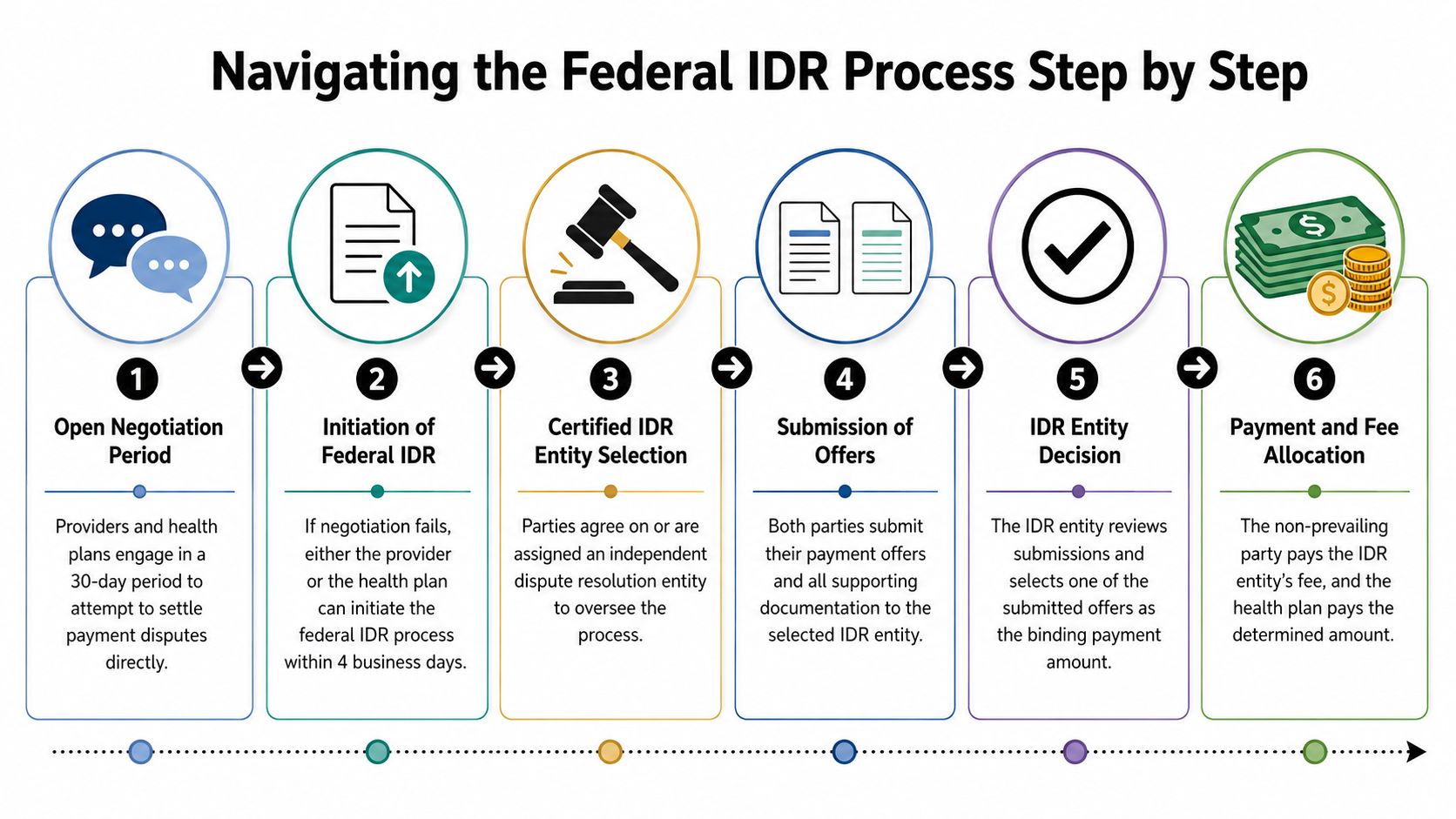

Navigating the Federal IDR Process Step by Step

Once a covered claim is paid too low, speed and sequencing matter. The federal process is timed tightly enough that loosely managed follow-up will cost you recoverable dollars.

According to Brookings' overview of the No Surprises Act dispute workflow, the health plan must send an initial payment or denial within 30 days of service, the provider then has a 30-day open-negotiation window, and if no agreement is reached either side can escalate to binding IDR. That timing is why NSA claims need their own workqueue, not a generic appeals bucket.

Step one begins at payment posting

The dispute doesn't really start when leadership notices underperformance on a monthly report. It starts the day the payment or denial posts.

Your posting team has to answer three questions immediately:

- Is the claim NSA-eligible?

- Did the payer issue an amount that warrants challenge?

- Has the claim been routed into a negotiation workflow instead of standard collection logic?

If those questions are answered late, the rest of the process becomes reactive.

Open negotiation is not a formality

The open-negotiation period is often treated as a procedural box to check. That's a mistake. It's your first structured chance to show the payer that the claim has been reviewed, documented, and prepared for escalation if needed.

A disciplined negotiation packet usually includes the core claim record, payment detail, and a concise explanation of why the amount is insufficient. You don't need to flood the file with every internal document you have. You need to present a coherent reimbursement position and preserve the chronology.

The strongest IDR matters usually look organized before they ever reach arbitration.

Escalation only works if intake is clean

If negotiation fails, either side can move into federal IDR. At this stage, many practices discover that their records aren't arbitration-ready. Missing operative detail, inconsistent coding support, weak proof of service setting, and poor communication logs all make a claim harder to defend.

A useful internal workflow looks like this:

- Intake review to confirm the claim belongs in the NSA pathway

- Payment variance review to decide whether the dispute is worth escalation

- Document assembly to create one coherent case file

- Deadline control with calendar ownership assigned to a specific team or vendor

- Submission review before filing to avoid avoidable rejection or weak positioning

What administrators should monitor

You don't need every manager in the details of each filing. You do need a small set of operational controls.

| Control point | What to watch |

|---|---|

| Eligibility routing | Whether likely NSA claims are identified before patient billing |

| Posting workflow | Whether underpayments are flagged on receipt |

| Negotiation handling | Whether requests are sent promptly and logged consistently |

| IDR readiness | Whether documentation is assembled before deadlines tighten |

Specialties where this matters most

The Brookings analysis specifically highlights areas where patients generally can't choose the specific clinician or transport provider, including emergency medicine, anesthesiology, pathology, radiology, neonatology, and air ambulance. Those groups should treat federal IDR as a core reimbursement function, not an occasional legal event.

When administrators frame the process that way, two changes usually follow. First, staff stop seeing underpayments as routine annoyances. Second, leadership starts measuring dispute readiness as part of revenue integrity.

Building a Winning IDR Case With Documentation

Claims don't win in IDR because a provider feels underpaid. They win when the submission gives the reviewer a credible reason to select the provider's offer over the payer's offer.

Start with the QPA, but don't stop there

A critical part of any practical No Surprises Act summary is understanding the qualifying payment amount, or QPA. Early policy analysis emphasized that Congress intentionally used the QPA, defined as the median in-network rate, as a core benchmark in IDR rather than tying arbitration to a Medicare-based formula, as discussed in Georgetown CHIR's analysis of early NSA implementation.

That same analysis notes the Congressional Budget Office projected the NSA would reduce insurance premiums by 0.5% to 1.0% below trend in most years and cut the federal deficit by $17 billion over 10 years. For providers, the important takeaway isn't just budget policy. It's that the statute was built to influence reimbursement behavior across the market. Payers know that. Your documentation strategy has to account for it.

What persuasive files usually include

Strong submissions tend to be disciplined, not dramatic. Useful support often includes:

- Clinical complexity detail that shows why the service wasn't routine in execution

- Provider qualifications when training, experience, or specialty capability materially matter

- Setting and acuity context that clarifies why the patient encounter demanded the level of care billed

- Coding consistency so the clinical record and claim tell the same story

- Negotiation history showing the provider acted reasonably before escalation

Common weaknesses that hurt providers

The losing file is often easy to recognize. It may be technically complete, but it doesn't make a payment argument. It just restates the bill.

That's not enough. IDR requires a comparative position. You need to explain why your offer is more appropriate than the payer's position, including when the payer leans heavily on the QPA.

A few recurring problems:

- Template narratives that ignore case specifics

- Unsupported acuity claims with no chart-based backup

- Inconsistent service descriptions across claim, appeal, and submission materials

- Late assembly that forces staff to file whatever they can find

Documentation should be built upstream. If you start gathering your evidence after payment posts, you're already working from a weaker position.

Groups looking to sharpen their dispute posture should pay close attention to common payor tactics in IDR, especially how payer positions are framed around benchmark logic and procedural pressure.

The file should read like one argument

Think less like a biller and more like a case builder. Every document should support the same reimbursement theory. The chart supports the coding. The coding supports the offer. The negotiation record supports your reasonableness. The submission should feel internally aligned.

That's why the best-performing organizations don't isolate IDR from the rest of revenue cycle operations. They make claims dispute-ready before the payment fight starts.

Operationalizing NSA Compliance in Your Revenue Cycle

The NSA reaches almost every part of the revenue cycle. When practices treat it as a legal issue owned by compliance alone, leakage shows up in patient balances, delayed follow-up, and missed payer disputes.

Front end failures become back end write-offs

Registration teams now carry more financial risk than many organizations realize. If they don't capture the right plan information, service setting, and patient status, the claim may enter the wrong billing path from day one.

Scheduling and intake also affect uninsured and self-pay workflows. Those patients follow a different path from insured NSA-protected claims. If your front end mixes those categories, downstream teams spend time undoing errors instead of pursuing collectible balances or recoverable payer amounts.

Billing and posting need NSA-specific logic

General billing rules won't catch all NSA issues. The business office should have a way to identify likely protected claims, stop inappropriate statement generation, and route low initial payments into review before the account ages.

That usually means building operational triggers into your existing revenue cycle tools, clearinghouse edits, or workqueues. It also means your payment posting team can't function as a passive data-entry unit. They need escalation rules.

A practical control structure often includes:

- Protected-claim flagging tied to specialty, place of service, and network facts

- Statement suppression rules for balances requiring NSA review

- Underpayment review queues for initial payments that need negotiation analysis

- Ownership mapping so one team is accountable for timelines and documentation

Collections workflows need restraint

Old collection behavior creates problems fast under the NSA. Once a protected claim hits patient collections incorrectly, you don't just risk a refund. You damage patient trust and create internal cleanup work that pulls resources from payer recovery.

For groups using modern medical collections software, the primary question isn't whether the platform can send statements. It's whether the workflow can reliably suppress, segment, and reroute balances that belong in a payer dispute path.

Administrators should audit three handoffs

If I'm reviewing an operation for NSA risk, I usually focus first on the handoffs, not the policy binder.

Registration to billing

Did the protected claim get identified accurately?Posting to underpayment review

Did the low payment trigger action, or did it disappear into normal A/R?Billing to collections

Did anyone stop an invalid patient balance before it left the office?

Most NSA problems aren't caused by ignorance of the law. They're caused by weak routing inside the revenue cycle.

A Practical NSA Compliance Checklist

A good compliance program is visible in daily operations. If staff need to search through old memos to know what to do, the process isn't mature enough.

Use this list as an internal spot audit

Train by role, not by broad policy. Front desk, surgery scheduling, coding, posting, patient financial services, and A/R follow-up all need different NSA instructions.

Map which claims should be flagged automatically. Use specialty, service setting, and network status to identify likely protected claims before statements go out.

Review patient-facing forms and scripts. Generic financial responsibility language often survives long after the law changed. Clean up forms that imply broad patient liability where federal protections limit it.

Build a notice and consent approval process. Don't let individual departments create ad hoc forms or local workarounds.

Create a negotiation and IDR intake standard. Every disputed claim should require the same minimum package of billing, coding, and clinical support before escalation.

Audit initial payment review. If low payments are posted without structured analysis, you're likely losing recoverable reimbursement.

Separate insured NSA claims from uninsured or self-pay estimate disputes. They are not the same operational pathway.

Track payer behavior. If one plan repeatedly sends low initial payments on the same service lines, that pattern should shape staffing and escalation priorities.

Practical rule: Compliance is stronger when teams can show the exact workqueue, stop-bill rule, form version, and owner tied to each requirement.

What the checklist should produce

The result should be simple. Fewer bad statements, faster underpayment identification, cleaner escalation files, and less improvisation by staff. If your team still handles NSA matters through email chains and memory, the checklist hasn't turned into process yet.

Frequently Asked Questions About the No Surprises Act

The hardest NSA questions usually come from the gaps, not the headline rules. These are the issues that create the most confusion in practice.

Does the NSA cover ground ambulance bills

Generally, no. Public summaries often highlight air ambulance protections, but ground ambulances are generally excluded from federal surprise-billing protections, which means billing exposure may still depend on state law or payer policy, as explained in HealthInsurance.org's NSA glossary.

For providers, that means you can't assume all transport-related claims follow the same federal rules. Intake, billing, and legal review should distinguish ground from air immediately.

Does the law eliminate all patient financial exposure

No. Patients can still receive large bills for services that are outside plan coverage. That's an important limitation because many front-office conversations flatten the law into “patients can't be balance billed anymore,” which isn't accurate enough for operations.

The better script is narrower. Protected services under protected circumstances follow NSA rules. Non-covered services may not.

What about uninsured or self-pay patients

They don't use the insured-patient NSA payment protections in the same way. Instead, uninsured and self-pay patients rely on Good Faith Estimates and a $400 dispute threshold, according to the same HealthInsurance.org summary cited above.

That distinction matters operationally because many organizations incorrectly route all difficult patient-balance issues into one bucket. Insured NSA disputes and uninsured estimate disputes are different compliance paths.

Should providers rely on patient communication to solve NSA issues

Not if the claim belongs in the payer dispute track. Patient communication still matters, but it should be informational, not compensatory. Staff should explain the billing status clearly while the reimbursement issue is pursued through the appropriate provider-payer process.

What's the most common provider mistake

Treating the NSA as a billing restriction instead of a revenue recovery system.

When groups focus only on what they can't bill, they miss the other half of the law. Covered claims now require structured payer follow-up, negotiation discipline, and evidence-ready files. The practices that perform better financially usually have one thing in common. They moved NSA work out of ad hoc exception handling and into a formal reimbursement workflow.

If your team is still asking whether the No Surprises Act summary is mainly about compliance or collections, the answer is both. But the more useful lens for administrators is this: it's a rule set that forces the organization to get serious about underpayment recovery.

Providers that want stronger control over NSA compliance, payer underpayments, and IDR execution can work with RevGuard, a healthcare revenue protection firm built to connect specialty-specific RCM with enforcement-driven dispute resolution. When your team needs cleaner claims upstream and sharper recovery downstream, RevGuard helps turn compliance work into protected reimbursement.